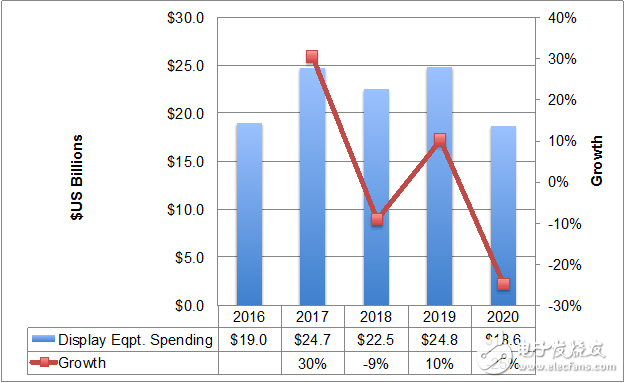

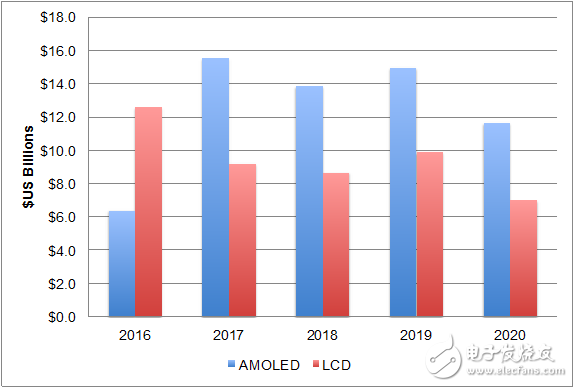

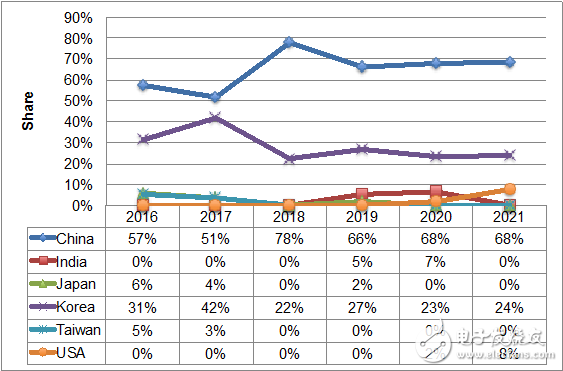

Display Supply Chain Consultants (DSCC) stated in the latest published display device report: 2017 is a year of excellence for the display device market, with revenues up 30% to $24.7 billion. As shown in Figure 1, the intensive investment in the OLED industry has driven OLED equipment capital expenditures up 143% to $15.5 billion, accounting for $15.5 billion. 63% of the overall display equipment capital expenditure market share, as shown in Figure 2. LCD equipment capital expenditure accounted for 37% of the overall display equipment capital expenditure market share, down 27% to reach 9.2 billion US dollars. Samsung is still the largest customer of the equipment factory, with a 54% increase of US$7.5 billion and a market capitalization of 31%. Samsung’s equipment capital expenditure on OLEDs accounts for 48%. BOE is the second largest display equipment manufacturer customer after Samsung. The market share of display equipment capital expenditure is 24%, an increase of 229% to 6 billion US dollars. At the same time, China's region is the largest equipment capital expenditure area in 2017, accounting for 51% share 42% of South Korea's share, as shown in Figure 3. The 6th generation line became a mainstream investment, accounting for 55% of the total, an increase of 52%. Figure 1: Display Equipment Spending and Growth Source: DSCC's Display Capex and Equipment Service Figure 2: OLED vs. LCD Equipment Spending Source: DSCC's Display Capex and Equipment Service Figure 3: Display Equipment Spending by Region Source: DSCC's Display Capex and Equipment Service In 2018, the capital expenditure of display equipment is expected to drop by 9% to US$22.5 billion. Although the booking of equipment is expected to increase by 5% to US$24.8 billion, capital expenditure will increase again in 2019. In addition to the capital expenditure of LCD, capital expenditure fell by 11% in 2018. In 2018, due to the delay in Samsung's investment planning, OLED capital expenditure decreased by 64% year-on-year. BOE is expected to replace Samsung's capital expenditure first position in 2018, up 12% year-on-year to 6.7 billion US dollars, and equipment capital expenditure will reach 30%. At the same time, LGD is expected to become the second equipment manufacturer customer, LCD The share of capital expenditure will increase from 27% to 39%, mainly due to a 22% increase in capital expenditure for 10.5 generation equipment. China's regional equipment capital expenditure is expected to reach 78% in 2018, up 37% year-on-year, mainly due to the government's support for panel production capacity of LCD TV and OLED Smartphone. At the same time, we expect China's region to lead OLED capital expenditures by 64% in 2018 to account for 36% of South Korea's market share. In 2019, it seems that BOE, Huaxing, LGD and Samsung have reached a peak spending in capital expenditures, at least in the capital equipment expenditure of 3.6 billion US dollars. OLED capital expenditure increased by 8%, and LCD capital expenditure increased by 14%. In 2019, it was a record year for equipment capital expenditure. Whether it is mobile phone application capacity investment or TV application capacity investment, LGD will lead the investment in TV application capacity. In 2019, compared with 27% of South Korea's market share, China's region still leads with 66% of equipment capital expenditure. However, in 2019, in terms of OLED equipment capital expenditure, Samsung will return to the position of leading manufacturer, ranking first with 24% market share, BOE 17% second, and LGD 16% second only to BOE. According to DSCC founder and CEO Ross Young, “The investment in production capacity in the display area from 2017 to 2019 reproduces an unprecedented scale of $72 billion, mostly from the investment in OLED production capacity and the high generation line of LCD. The investment of such a scale is basically unattainable without the subsidy and support of the Chinese government, and this will also trend suppliers of the panel manufacturers to provide more excellent cost solutions. In the long run, consumers It will also benefit from increased capacity and drive down costs and product prices." vape world wholesale,wholesale pop disposable,e-cigarette wholesale,vape pens wholesalem,chinese vape suppliers Shenzhen Aierbaita Technology Co., Ltd. , https://www.aierbaitavape.com